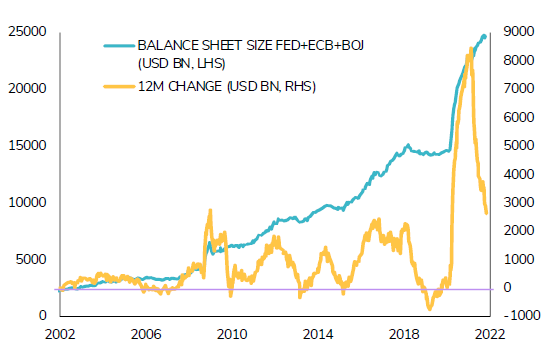

To the surprise of many, this blue-sky scenario hasn’t calmed the hyperactivity at central banks and governments. The Federal Reserve continues to hold US interest rates at 0% and continues to expand its balance sheet. US money supply has increased nearly 40% since 2020, its largest ever two-year increase. The US Federal Government continues to borrow and to spend trillions of dollars despite a looming debt ceiling. Most developed countries and central banks are following the US, with monetary base expansion, fiscal stimulus and ever-increasing debt levels.

As we enter a new year, the question for investors is whether the ‘goldilocks’ market and macroeconomic conditions in place since the second quarter of 2020 will continue. The current balance looks rather fragile. The global economy should not overheat, keeping key policy rates on hold, but should be strong enough to avoid sparking recession fears.

We believe that the worst of concerns about stagflation have mostly been priced into markets. We expect slower, though above potential, global economic growth in 2022. Ironically, some downside surprises to growth may be good news for investors. While inflation might stay sticky for a while, lower-than-expected growth will let central banks keep interest rates low in 2022. This would be positive for risk assets. We also expect earnings growth momentum to remain a tailwind for global equities.

While this ‘goldilocks’ scenario means that we favor an overweight stance on risk assets, we also believe that volatility may rise next year as markets face some downside risks. We call them the ‘three bears’ and the appearance of any one may trigger a meaningful market decline.

The first ‘bear’ is China. Its regulatory crackdowns should continue through 2022. In addition, we do not believe the Chinese authorities have any appetite to engineer a re-acceleration of growth. As such, China may continue to disappoint next year and weigh on global economic growth, perhaps a little more than expected. The delayed effects of deleveraging some parts of their economy, for example in real estate, also create an elevated risk for markets.

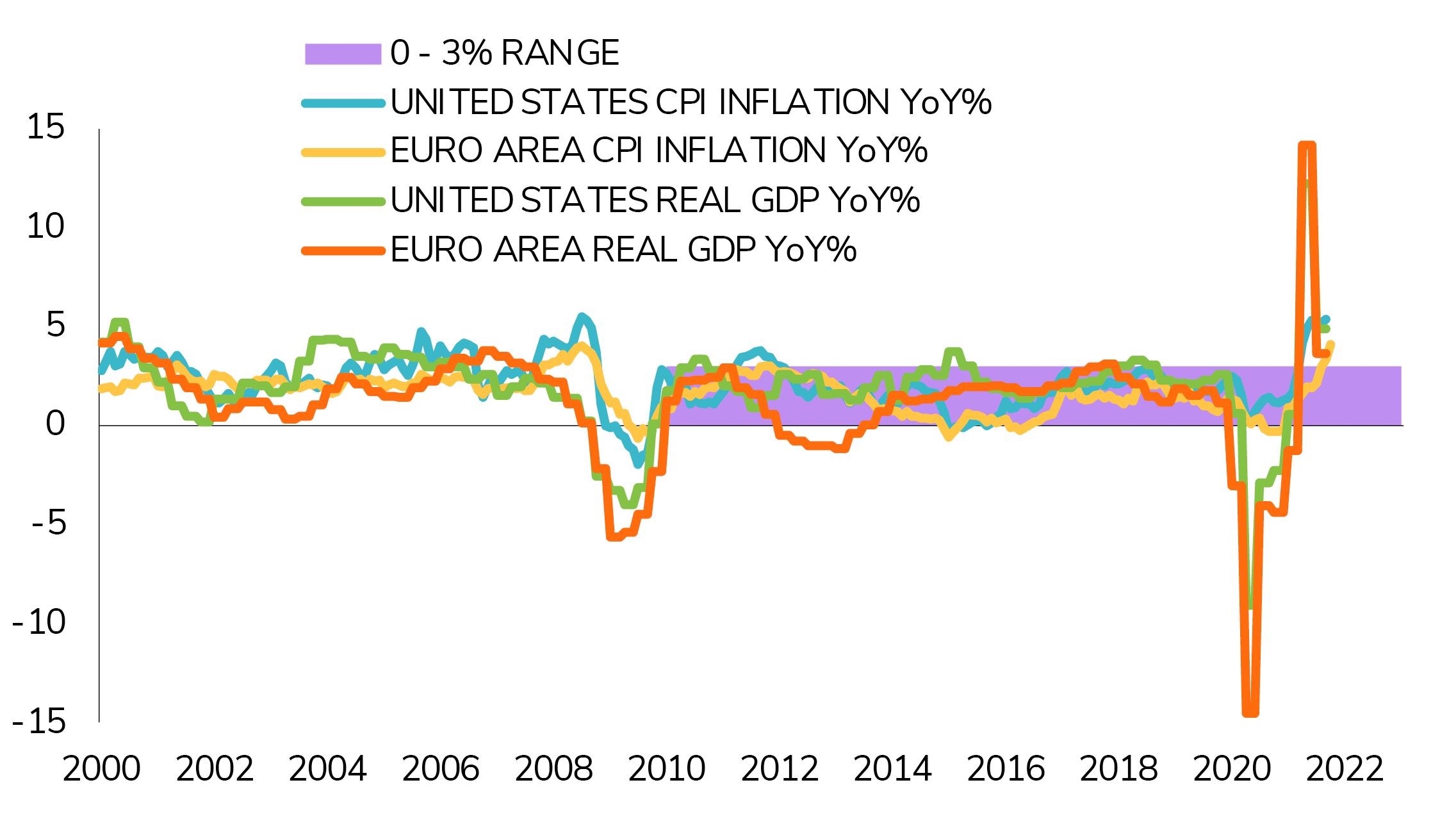

The second ‘bear’ is stubbornly high inflation. Supply bottlenecks and labor shortages have pushed inflation expectations to high levels in 2021. Persistent inflation would undermine purchasing power and consumer sentiment. While downward revisions to growth and production normalization reduce the risk of an inflationary spike in 2022, the longer inflation stays high, the more it becomes selffulfilling and puts the global economic recovery at risk.

The third ‘bear’ is a potential policy mistake. As we all know, the current equity bull market remains - to some extent - dependent on monetary and fiscal policies. Global central banks sound slightly less dovish and global fiscal policy has shifted to a tightening mode. While we believe that the market should be able to absorb a small and gradual monetary policy adjustment, the current context does not leave much room for a policy miscommunication. On the fiscal front, there is also a risk of disappointment, and a growing threat of another US debt ceiling.

We remain convinced that our disciplined and nimble investment approach will prove effective in helping our clients to achieve their risk-adjusted return targets. We also believe that the current macroeconomic environment of ample liquidity and creative disruption generates outstanding opportunities for investors on at least two levels. First, the world is going through an extraordinary period of innovation, in technology, healthcare, energy transition and many other sectors. A handful of industries and companies are being disrupted, paving the way for winners and losers. The second area of opportunities lies with market dislocation. A very high level of financial leverage, over-optimistic expectations and expensive valuations will spur market volatility and trigger some forced sell offs. This will create exceptional alpha opportunities for astute investors.

We wish you happy New Year and look forward to continuing the discussion with you in 2022.