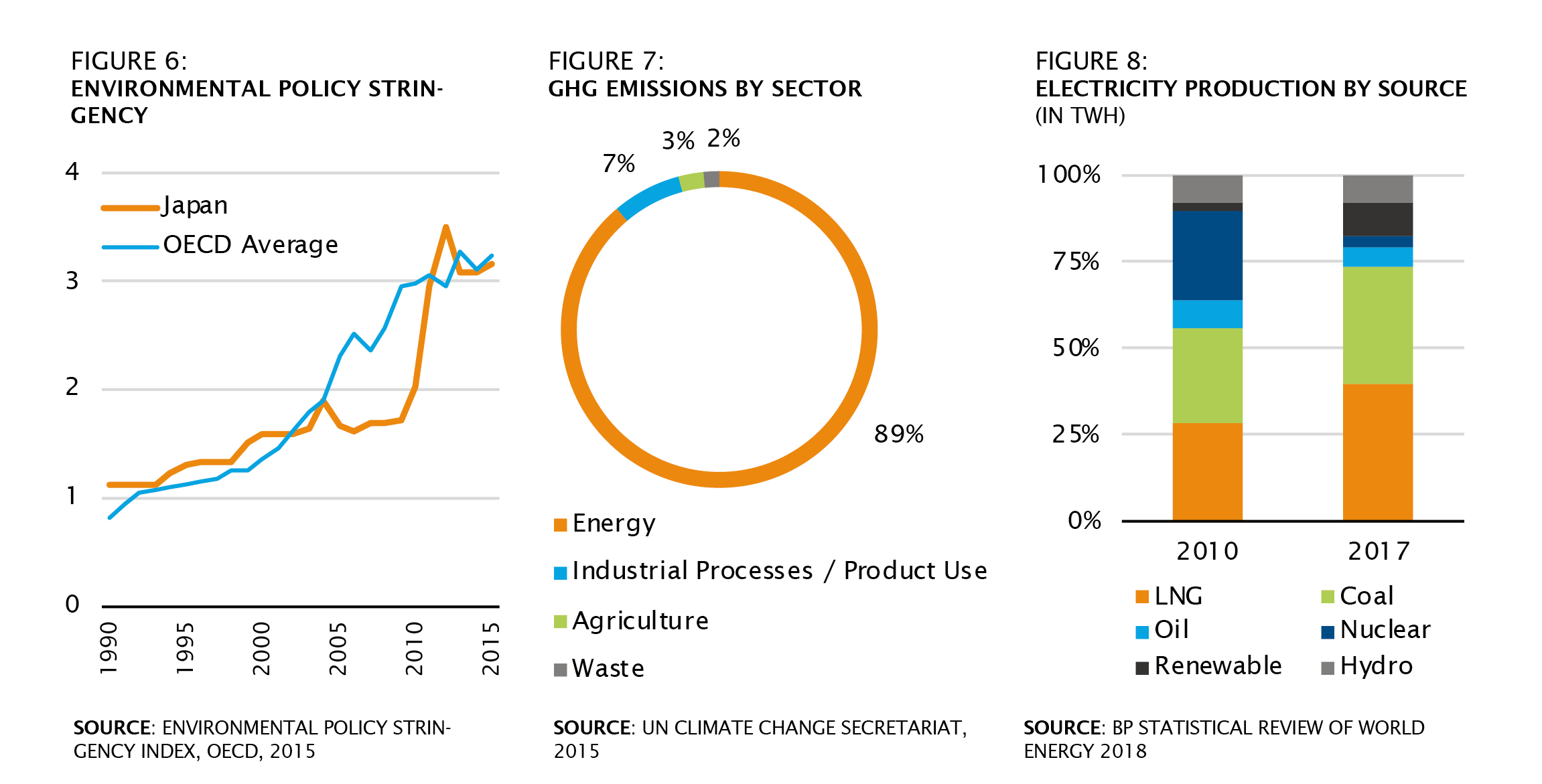

The E of ESG looks at the financial and reputational risks linked to companies’ impact on the environment. With awareness of climate change and other environmental issues growing, consumer behaviour is shifting and environmental legislation has been increasing in Japan and elsewhere, as we can see in the chart below.

This trend of increasing regulation means that polluting is becoming more expensive. As more and stricter regulation is being created, the financial burden of a company’s environmental impact will shift from the public to the firm.

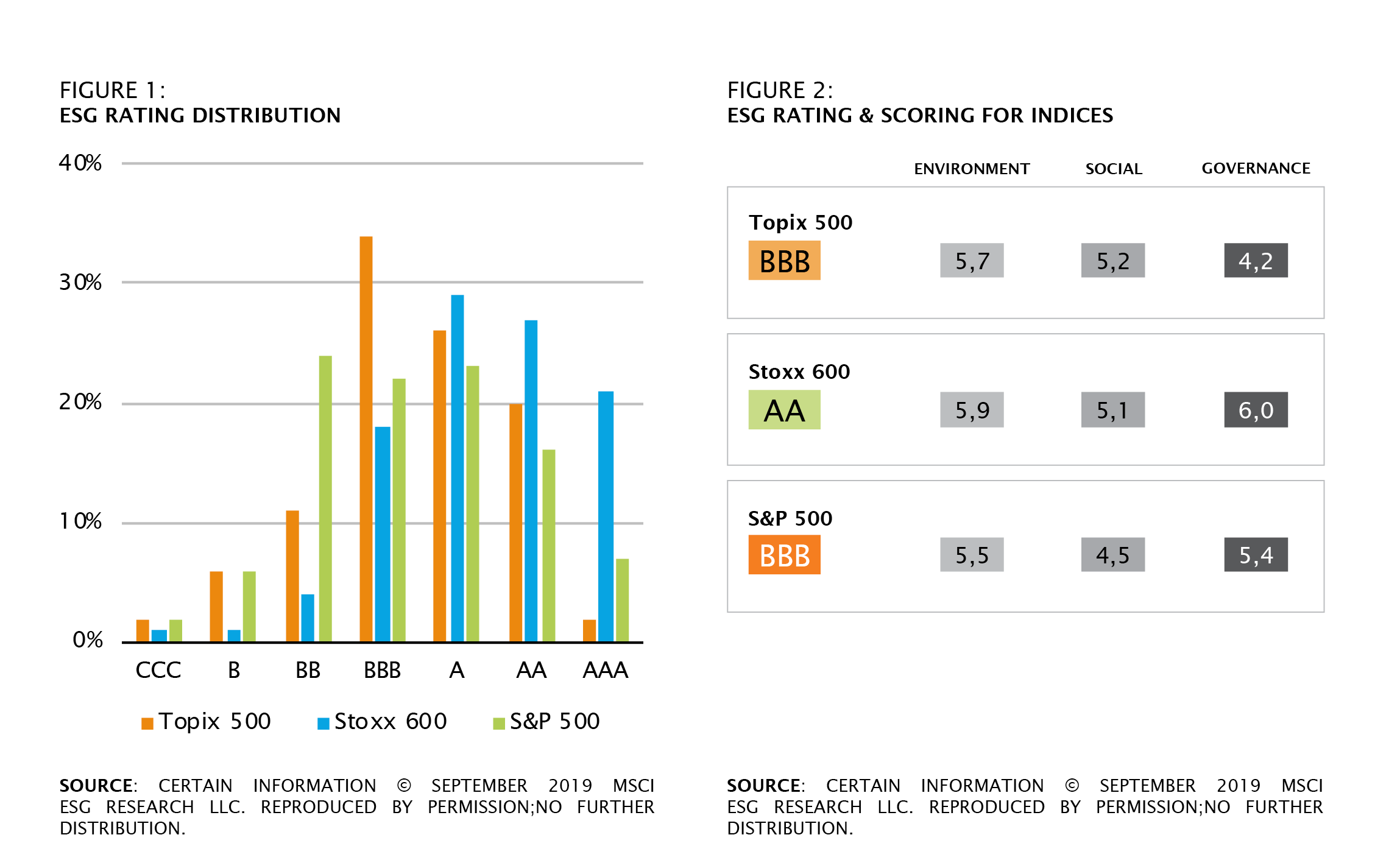

On environmental issues companies tend to do a little worse than their European competitors but better than American companies. Their emission of regulated substances (e.g. NOx, SOx, VOC) tend to be low in international comparisons and they produce comparatively little waste going to landfills. However, the latter is due to a high degree of thermal recycling (i.e. burning vs. storing), both having different environmental issues. In regards to natural capital management Japanese and US companies considerably lag European ones. They use less sustainably produces raw materials (e.g. palm oil, wood, etc.), have less transparent supply chains, and face higher of water scarcity related risks.

On climate change the Japanese company’s efforts seem to be comparable to their international competition. However, unlike the EU, Japan does not yet have a comprehensive carbon pricing scheme. As the country is projected to miss the targets necessary for the maximum 2°C temperature rise set by the Paris Agreement, Japan’s environmental ministry is deliberating carbon pricing. It now seems to be more a question not of if, but when, such a scheme is implemented, and how comprehensive it is. The academic consensus for the necessary worldwide price of carbon to reach the goals of the Paris Agreement is USD 40–80 / tCO2 by 2020 and USD 50–100 / tCO2 by 2030. For some companies such prices would ruin their business model, making them unsustainable investments.

Industries with high carbon emissions and low mobility (in the sense that they have little chance of transferring their operations out of the regulatory jurisdiction) are at the greatest risk of being subjected to carbon pricing rules. Some examples for this are the utility, energy and materials sector.

Almost 90% of Japan’s greenhouse gas emissions stem from energy-related activity, among the highest levels of industrial nations. A major source of emissions is electricity generation because Japan relies heavily on fossil fuels, particularly since nuclear power plants were shut down after the Fukushima disaster in 2011. Currently, around a third of Japan’s electricity is produced by burning coal, which is highly greenhouse-gas-intensive. Coal is in fact the second biggest source of electricity, only exceeded by liquefied natural gas, which emits about 40% less greenhouse gas but is more expensive than coal.

Coal’s relative cheapness is the reason it remains a major source of energy in Japan. Without carbon pricing, pricing pressure and capital expenditure requirements are preventing a shift to environmentally friendlier energy sources. And this has been apparent in our discussions with electricity utilities: many say they would like to become more environmentally friendly soon, but the economic reality makes this difficult. In capital- and energy-intensive industries like electricity utilities, significant environmental improvement is dependent on the implementation of policy that shapes market conditions to encourage change.

There is currently a somewhat confusing situation in Japan in that on one hand the environmental ministry says it is working on a carbon pricing scheme, while on the other the ministry of economy has identified thermal coal as a key industry for promotion and is factoring it into its long-term plans. Accordingly, utilities are trying to transition slowly to liquefied natural gas due to the risk of carbon pricing hitting their coal plants, but the contradictory messaging from government has slowed this process.

This dilemma is shared by companies across industries. For example, they may replace a few old boilers with more efficient ones one year, and work on saving energy another. The philosophy is one of slow but steady improvement (kaizen). Sweeping, disruptive change is not seen as feasible because it would destroy a company’s profitability, increase its cost of capital and eventually result in bankruptcy. That said, this approach is insufficient to achieve the goals of the Paris Agreement and a policy intervention will become necessary. From an investor’s standpoint, awareness of policy trends and assessing the risks they involve is vital to weather the carbon transition.