We are very glad to announce that last June we received the prestigious 2019 HFM European Award Fund of Hedge Fund specialists for our fund of funds with an Uncorrelated strategy. In 2019, this strategy continues to outperform its peers. In the current environment, where portfolio diversification has become even more challenging, we are convinced this product makes sense.

The hedge fund industry and our products performed very well in the period under review, outperforming, more specifically, equity markets. The main contributors were our trend followers, macro discretionary and multi-strategy multi-portfolio managers’ allocations. Consequently, it makes this a great year for our products, with the best first eight months since 2009.

We have changed our strategy views by reducing the Equity Hedge and Event-Driven funds. The main reasons are a strong up-trending US equity market since the beginning of the year and increasing volatility. With a less accordant FOMC, trade war, Brexit and Middle East crisis, the recent increase in volatility is expected to be here to stay. In this context, we have reallocated a part of our Equity Hedge allocation to Convertible Arbitrage. The latter could take advantage of this environment while keeping a foot in the equity market. A favourable corporate action pipeline and an improvement in US new issuances, thanks to a new tax law, potentially support this strategy as well, a case developed in detail at the end of this document.

Additionally, as well at the end of this document, you will find a special case on the opportunity set for agency MBS arbitrage.

- The rally in governemental bonds supported discreationary and systeamtic managers

- Managers’ consensus now points to a downturn cycle

- Equity markets saw a great sector dispersion in overall flat US markets

- Activist strategy was the poorest startegy in the review period

- Multi-credit managers have increased their distressed and short high yield allocation

The situation so far

Macro

The review period was quite supportive to discretionary macro strategies, particularly in June, namely European long duration & US inflation, and in August, as we witnessed sharp flight to quality, beneficiary to Long bonds and defensive trades such as Long Gold. Notably the August primary surprise in Argentina triggered a massive repricing reinforcing the govies rally initiated in May. While risk budgets are still in their lows, managers were unable to assess markets, tetanized by conflicting forces such as macro risks (i.e. Trade war, Brexit, Hong Kong protests,…), a dovish Fed with a 25bps rate cut in August and markets rallying on Trump’s raging tweets. Managers’ consensus now points to a downturn cycle and most tilted portfolios toward long govies, and turned overall negative equities and long gold as well.

Regarding trend followers, the period was outstanding, benefiting from Longs in Equity and Bonds, equally weighted, allowing most to post record profits YtD and erase long time drawdowns. The picture for macro systematic was more contrasted, in either short or long-term trading horizons, relative value models in bonds and equities reacting negatively to the sharp turn in risk sentiment while some managers were more resilient, particularly in June, thanks to their equity based models.

Our outlook

The first cut in US rates in now over 10 years initiated the perfect storm for discretionary macro and trend follower managers, having tilted allocation to Long bonds for a couple of months, their pre-crisis golden goose. Indeed, the market uncertainty is growing and the market dynamic is gradually shifting from equity-driven to a recession environment, given the characteristic inverted US yield curve. Nonetheless, we reiterate, again, our preference towards relative value models exclusively focused on Rates/FX and will avoid any outright equity and credit, as these are embedded throughout our allocation to systematic managers, especially with trend-following models.

Equity hedge

May to August was a tricky period for equity markets with great sector dispersion, powered by the rally in bond markets. The US 10y yield fell gradually from 2.5% to 1.5% in a straight line, anticipating lower growth with no pick-up in inflation in the US. In that environment, bond-proxy equity sectors like Utilities, Real Estate and Consumer Staples outperformed substantially cyclical ones - Energy, Financials and Industrials—in an overall flat US equity market. Market neutral strategies did better globally than directional strategies in this apparently trendless market. Many net long biased managers tended to stay invested in momentum growth Information Technology and Communication Services companies that held pretty well in this environment. However, we saw some longer term long biased managers reducing their net and gross exposures prior or during the yield curve inversion in the US, as it has often been a warning signal to tougher times on markets.

Our outlook

We expect a challenging last part of the year on equity markets after a bullish start and a consolidation period. We will continue to favour managers with a short-term trading mentality and conversely, managers with a long-term investment horizon that look behind the short-term noise.

Event driven

In this second 4-month period of 2019, Event-Driven strategies posted quite disparate performances with only merger and credit arbitrage being positive in an environment of flattish yet volatile equity markets and rallying bond markets.

Again, distressed/restructuring funds, particularly those with an allocation to Emerging Markets, struggled over the period.

After being the best performing strategy over the 4 first months of 2019, activism was the poorest performing strategy, as managers, who tend to hold concentrated and net long exposures to equities, had a higher down market beta than up market beta.

Continued concerns over the US-China trade dispute and IPOs were detrimental to performance earlier in the period, particularly for special situations and merger arbitrage. June showed promising M&A activity for merger arbitrage with highest new deal volume and number of new deals since 2011, potentially announcing a new wave of M&A. Although this activity was sustained into July, the rest of the period was pretty quiet.

Our outlook

The current trade war and Brexit uncertainty environment continues to weigh on key economic metrics such as exports and manufacturing. The CEO Confidence index is nearly back to pre-Trump election levels and cautious corporate activity can be expected with a heavy political agenda ahead.

Trump election’s euphoria fading slowly away

Relative value

The review period was quite supportive to discretionary macro strategies, particularly in June, namely European long duration & US inflation, and in August, as we witnessed sharp flight to quality, beneficiary to Long bonds and defensive trades such as Long Gold. Notably the August primary surprise in Argentina triggered a massive repricing reinforcing the govies rally initiated in May. While risk budgets are still in their lows, managers were unable to assess markets, tetanized by conflicting forces such as macro risks (i.e. Trade war, Brexit, Hong Kong protests,…), a dovish Fed with a 25bps rate cut in August and markets rallying on Trump’s raging tweets. Managers’ consensus now points to a downturn cycle and most tilted portfolios toward long govies, and turned overall negative equities and long gold as well.

Regarding trend followers, the period was outstanding, benefiting from Longs in Equity and Bonds, equally weighted, allowing most to post record profits YtD and erase long time drawdowns. The picture for macro systematic was more contrasted, in either short or long-term trading horizons, relative value models in bonds and equities reacting negatively to the sharp turn in risk sentiment while some managers were more resilient, particularly in June, thanks to their equity based models.

Our outlook

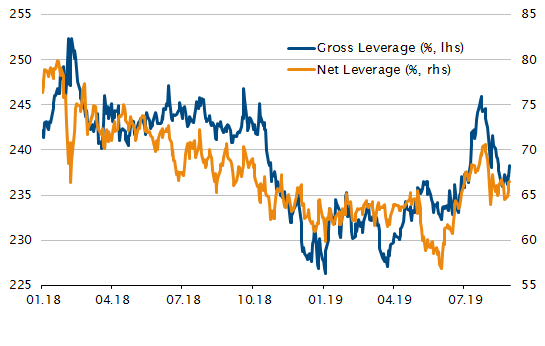

One of the cornerstones of the Relative Value silo is leverage and it would seem hedge funds cannot access the same leverage that they did pre-crisis. Bank collateralization (including financing) is better, high yield spreads could be considered to lack signs of stress, margin to-equity and general exposure is well off the 2017 highs, and arbitrage funds size does not appear to be too large. Aligned and adequate for the risk implemented by our arbitrage managers, in their highs, we maintain our positive outlook for the segment while trimming down any beta components across capital arbitrage, using convertibles as defensive directional tools. Notably, we see an ever growing opportunity set for agency MBS.

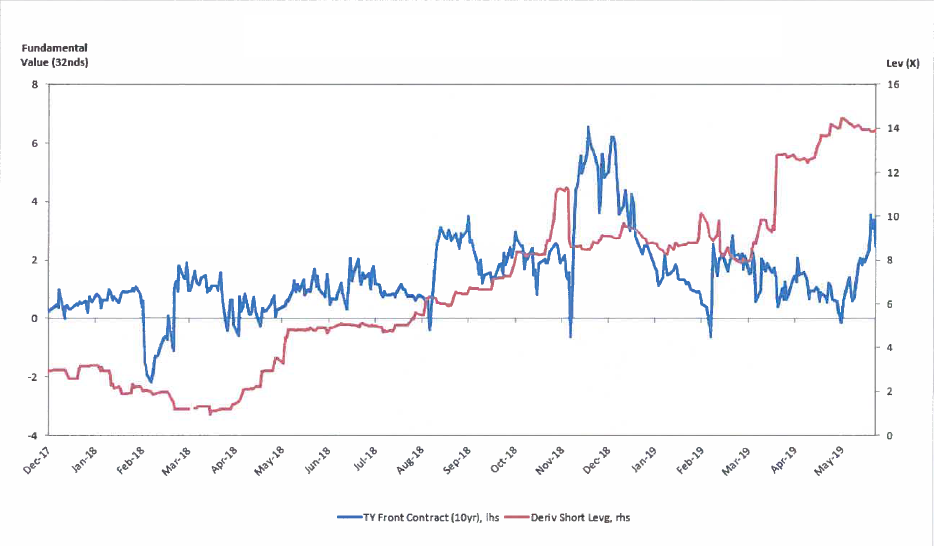

10 YEARS CONTRACTS - RISING OPPORTUNITY

Our convictions

How to keep some beta in an end-of-cycle environment

Navigating the current environment is quite complex, despite double-digit equity market returns and over nine years of accommodative monetary policy, which have generated plenty of opportunities. Equities are at their highest, spreads at their lowest – even after last year’s correction – and US rates were once again cut, with a dovish Federal Reserve. Many were forecasting a quick normalisation, but the macro environment is torn between offsetting forces, including political issues such as Brexit, the trade wars and the Venezuelan crisis, conflicting economic data and lagging inflation.

As seasoned fund of hedge fund managers, our primary goal is to meet return and volatility targets, while abiding by soft and mandatory guidelines. One of the main issues we have faced since the implementation of accommodative monetary policies has been finding managers that are aggressive enough in an environment of depressed volatility.

In this situation, the simplest and most logical choice, other than increasing leverage, would be to allocate to directional, beta-driven managers, namely running equity L/S and event-driven strategies and, marginally, credit L/S strategies. The trade-offs would be the downside in case of a sell-off and timing towards the end of the cycle, which could be detrimental. Instead, we have opted to increase our allocation to convertible arbitrageurs.

We have added risk since a couple of years to convertible arbitrage managers because we like the hybrid equity and bond nature of convertibles, as well as their embedded long convexity profile. Investors tend to see convertibles as a pure market hedge exhibiting a long-volatility profile. But the reality is more nuanced, with the credit component creating a short-volatility exposure. Indeed, a lack of credit buyers makes the option credit sensitive, which can lead to ‘risk-off’ cheapness.

This segment of the market has radically changed since the crisis, where it was initially driven by proprietary desks and hedge funds. Now, over 70% of market participants are long-only funds which have other objectives and do not price volatility. This has shifted the market from managers providing liquidity to managers tracking beta. Nowadays, the market is biased towards US, large-cap, healthcare, IT and equity-sensitive issuances. The hedge fund managers still active in the segment are not legion, as 2008 pushed many out of the market. The bulk of these remaining managers have drifted from their core skills in convertibles to allocating across the capital structure, including to outright credit, credit arbitrage and relative value equity, such as event-driven and M&A.

The way convertible arbitrage trading is strictly implemented differs across the capital structure, with different targets and delta. There are essentially four approaches: Distressed/high yield trading – These bonds have a high default probability and the embedded option is significantly out-of-the-money. The stressed and distressed positions play out either through a recovery in the issuer’s financial position or in a bankruptcy, while those not distressed target yield with a focus on fundamental credit and equity.

Bond floors (short duration out-of-the-money calls in safe credits) – This approach looks for corporate action, exchanges and oversold stocks that may appreciate due to earnings surprises, M&A or other events, but have limited downside risk.

Volatility trading – This approach seeks to constantly modify the hedge ratio – the amount of stock sold short against the convertible bond – based on an assessment of the embedded option’s implied volatility. In addition to delta trading, hedge funds can try to capture additional profits by gamma trading – trading the underlying stock as delta changes. This is the most crowded segment by the long-only players, as embedded options are significantly in-the-money.

Equity-like trading – This option is deep in–the-money, typically involving a high hedge ratio which can approach 100%, and trades such as a synthetic put on the stock. The segment often exhibits an inverse correlation and beta to equity markets, and is characterised by investment approaches ranging from exchanges and repurchases to synthetic puts, as the managers focus on low-premium bonds.

Our focus is on managers with a defensive profile, a moderate gross exposure, delta in the 60s and duration as low as possible, to mitigate interest rate sensitivity. Most managers are deploying their entire risk budgets and increasing their volatility bucket. They are optimistic about the current environment, which is benefitting from a confluence of supportive factors. Indeed, valuations are fair, there is a supportive buyers base, convexity is attractive, and we are still seeing a good level of M&A activity. Nevertheless, we must weigh this up against potential challenges the segment could face, such as a sudden rise in rates or a sharp widening of credit spreads due to macro uncertainty – the list is not exhaustive.

Securitised products – stick to agency residential mortgages

Just like in the period preceding the financial crisis, securitised products and more complex strategies are making a comeback. The segment, which is split across residential MBS, commercial MBS and ABS, has steadily outperformed other hedge fund strategies since the last 2011 credit correction. While it did not get a lot of traction for long, it is now back in the spotlight.

As there are many developing stories in the space, below we have tried to outline some tools to help investors navigate US residential markets. The major factors at play are that US housing markets have finally rebounded from 2012 lows, and unlike many other US asset classes, residential securities are still trading cheaper than at their last peak levels. More severe ratings and demanding regulatory constraints have forced investors out of these markets, triggering additional arbitrage opportunities.

Residential MBS can broadly be split across agency and non-agency mortgage securities, two notions which require some explanation. The key characteristic of the former is the underlying loans conform to agency guidelines – the agencies being Fannie Mae, Freddie Mac and Ginnie Mae. Fannie Mae and Freddie Mac focus on mortgages of a certain size, originated through private-sector programmes and generally referred to as conventional conforming loans, while Ginnie Mae focuses on loans originated under Federal programmes.

These agencies bear the embedded credit risk of any loan they issue, and the key risk for all three is prepayment. This is also the primary source of difference in fundamental value among agency MBS. Fannie Mae and Freddie Mac were placed into conservatorship in 2008 by the US treasury in order to survive the crisis. This created additional securitisation, particularly through the emergence of credit transfer mechanisms to the private sector.

In general, the agencies segregate loans into pools according to property type, payment schedule, original maturity and loan coupon rate, to create a standardisation of the segment, which represents the largest and most liquid part of the MBS market. Today, more than 90% of agency MBS trading occurs in the to-be-announced (TBA) forward market. In a TBA trade, the exact securities to be delivered to the buyer are chosen just before delivery, rather than at the time of the original trade.

Regarding the non-agency market, the underlying loans typically do not conform to agency guidelines. It is a large and diverse spectrum across three categories: prime or A credit, then alt-A and finally sub-prime credit. Without going into the details, discrepancies range according to size, issuer, quality or interest rate. While historically, trading has occurred on legacy issuances pre-2008, we are increasingly seeing the securitisation of non-agency credit, with a resurgence in new issuances, which is quite worrisome.

Without addressing all the sub-strategies and derivatives used within the segment, one recurring theme we find appealing is the MBS basis trade. It has represented the bulk of the risk since the crisis, with managers allocating tactically either long or short. Many have been unsuccessfully short (i.e. short agency MBS vs. long US Treasuries), as they forecasted quick balance sheet normalisation and an end to the MBS repurchasing programme following the end of the Fed tapering in 2014, but this has only occurred recently.

Since the crisis, the recovery of the non-agency market – still only a fraction of the agency MBS market – is growing and providing opportunities. However, the segment is a no go for us, due to the ever-increasing securitisation and new issuances, given most of the P&L post-2008 came from legacies and lacklustre liquidity. Regarding agency MBS, the opportunity is once again gaining traction – spreads are wider, there are regulatory tailwinds, and the Fed is out of the way. The Fed has dominated the market for ten years, buying almost $2trn MBS; now it is gone, which should lead to opportunities for years to come as the market adjusts. The uncorrelated profile of the segment also makes it an interesting portfolio management tool.

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document. (6)