Few other asset classes have suffered as much as emerging equities and currencies this year. The MSCI Emerging Markets Index is down by around 17% year-to-date in US dollar terms, compared to the MSCI World Index (US dollar terms) that held fairly well until the end of third quarter of the year and is now down by around 7% year-to-date.

Focus

Emerging market equities: opportunity amid challenges

Wednesday, 12/19/2018While global markets continue their emotional ride, we feel there is value to be found in emerging market equities. We tweak our views to more positive given solid long term growth prospects and sharp valuation dislocations present in selected emerging markets.

Shoaib Zafar

Analyst

- 2018 has been a challenging year for emerging market equities, but that could be about to change

- A permanent resolution to the US-China trade-dispute, a more dovish Federal Reserve and a falling oil price could all act as positive catalysts for the asset class

- We see interesting opportunities at attractive discounts across the emerging equity universe, and especially in China, Brazil and Russia

“In our view emerging equities look attractive at their current oversold levels as there are some positive catalysts in sight.”

Have emerging equities fallen too far this year?

Returns of selected emerging markets vs. the MSCI World (USD, year-to-date)

Source

Bloomberg, US dollar terms. Date as of: December 2018

What began as a seemingly healthy correction in high-flying emerging-market stocks during the spring became much more serious as the year progressed, with firms involved in the smartphone supply chain (Hong Kong, South Korea, Taiwan), the autos sector (China, India, South Korea), and domestic consumption plays (China, India), all suffering badly year-to-date. A combination of factors played into that. A stronger dollar, rising interest rates in the US, worries on global debt service costs, trade-disputes, a political stand-off between the US its ally Turkey, and then fears of a slowdown in China.

Unless there is a global recession, in our view emerging equities look attractive at their current oversold levels as there are some positive catalysts in sight: most importantly, a trade settlement between the US and China and the Fed slowing its rate hikes. The sharp recent fall in crude oil also helps energy importers such as China and India. With emerging equities trading at a discount of around 30% to global markets, current valuations are perhaps pricing in the challenges facing emerging markets, but not their possible solutions.

What’s more, since their last full-fledged financial crisis in early 2000s most emerging economies have learnt some important lessons. Most are much better diversified now than two decades ago and many have accumulated sizeable reserves. Their central banks are more credible, and states like China have learnt how to tame inflation by steering fiscal policy.

Let’s consider some of the issues that emerging markets are currently facing.

Trade waRs are a negative-sum game

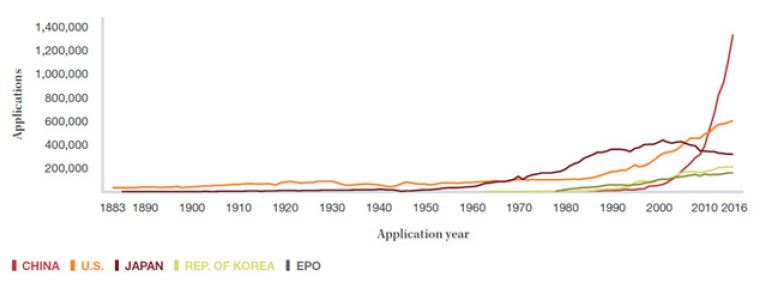

China exports to the US goods and services in value about four times the reverse trade amount, and that too represents only c.4% of China’s GDP. The export-driven economy has been able to maintain a positive trade-balance (though shrinking lately) with most trade partners. Savings generated have been fueling local growth, industrial subsidies, a fast development of Intellectual Property (making China the top patent filer globally, chart below), a shift towards a consumer-oriented economy and notably China’s growing geo-political weight.

Trends in patent applications for the top five filing countries

Note: EPO is the European Patent Office. The top five offices were selected based on their 2016 totals.

Note: EPO is the European Patent Office. The top five offices were selected based on their 2016 totals.

Source

WIPO. Date as of: September 2017

On the other hand, it exposes China to criticism from its trade partners especially the US. From criticizing China over its trade, currency management and Intellectual Property (IP) rights practices, President Trump’s administration shifted this summer to material punishments in the shape of trade tariffs. So far, USD 250 billion of Chinese goods have been included on a list of trade tariffs, and President Trump continues to threaten China with further tariffs. The situation could go either way from here, with tariffs either being slapped on all Chinese exports to the US (USD 500 billion of goods) or being reduced significantly. But we feel that the likelihood of a sustainable settlement to the dispute is high.

That is in part because the Chinese seem to realize that they are the biggest potential losers in a negative-sum trade war with the US, and so their response has been relatively contained and targeted carefully. For instance, they have imposed tariffs on soybeans, which are a key output of some of the states that voted for President Trump. What’s more, they’re under pressure from other trade partners to make sizeable concessions. Meanwhile, the last-minute NAFTA deal in September showed that President Trump’s economic advisors are mindful of the dangers involved in prolonging the trade disputes.

Following the latest temporary truce reached at the G20 meeting in November, we believe that sooner rather than later the two countries should be able to iron out their difficulties on a permanent basis. Such an outcome would be welcomed by the financial markets.

How US rate hikes will affect indebted emerging markets?

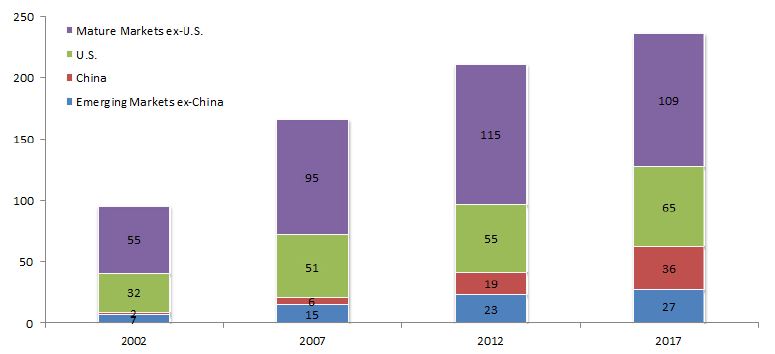

The IMF’s Institute of International Finance (IIF) reports that total debt (not just sovereign bonds) outstanding in emerging markets rose by around 40% over the past decade. And yet emerging markets still only account for around a quarter of the USD 240 trillion of debt outstanding around the world.

Total Global Debt - all sectors (USD trillion, Q4 of each year)

Source

IIF Global Debt Monitor. Date as of: October 2018

As rates cycle turns and liquidity becomes scarcer, debt servicing costs will rise for both indebted emerging and developed markets – albeit by varying amounts. This is why the Fed’s hawkish comments in October led to an upward readjustment of developed markets’ risk premium and volatility to spike in US equities. But will the Fed remain hawkish as US growth moderates and pressure increases on wages and margins? Especially after its latest December hike? If it does, it might risk causing a recession. We believe the Fed has reached an extended pause.

Lower oil prices beneficial for the emerging market bellwethers

Oil prices have fallen sharply by around 30% over the past two months, and that’s highly beneficial for major emerging markets that have to import oil such as China and India as it’s likely to result in improved current account balances, more stable currencies and lower inflationary pressure. This eliminates the need for their states to intervene with fiscal or other measures to prevent economic growth from derailing.

Finding opportunities throughout the emerging world

Let’s consider some of the investment opportunities within the emerging world at present.

Russian equities, for instance, are currently trading at fairly cheap valuations: their 5x forward P/E represents a hefty discount to their own historic average and to the current emerging market average of 14x. An oil exporter, Russia has some of the lowest breakeven oil production costs in the world and major oil companies like Rosneft, Lukoil and Tatneft are well placed to maintain and grow oil output at a price below USD 30 per barrel. So even though oil has been weak recently, this is unlikely to result in higher volatility in earnings for the sector, which accounts for slightly over 30% of Russian’s GDP and 70% of its exports.

In Chinese equities, a trade settlement with the US could spur an immediate rebound in sectors including financials and consumer discretionary. As we are cautious about the country’s debt situation we will seek out unlevered companies, which can be found in many sectors. We prefer a diversified exposure, investing selectively in firms with strong fundamentals and prudently managed balance sheets. Growth names in consumer discretionary such as Haier Electronics and Anta Sports and more defensive firms such as Guangdong Investment in utilities tick all the right boxes.

The Indian economy has been protected from trade wars and has been recovering in 2018 after two difficult years (demonetization in 2016 and General Sales tax in 2017). However, Indian equities trading at 19x forward earnings represent an unusually high premium over their emerging market peers’ average and their own historic levels. This makes us believe we can find better value elsewhere in the emerging universe.

On Brazil, the current focus has been on the market-friendly outcomes of the recent elections. While there remains a delivery risk given high expectations from the new President – especially fiscal and pension reforms agenda – financial markets seem prepared to generously reward any positive outcomes. The country’s banks should be big beneficiaries of increased economic activity and lending, and a fall in provision expenses over the past two years has supported their bottom-line growth. Today, the three largest banks – Banco do Brasil, Banco Bradesco and Itau Unibanco – are sitting on CET1 reserves comfortably in excess of the requirements for 2019.

Turkish equities have been recovering since the easing of the sanctions imposed by the US.. Further improvement in political stability and economic visibility could support both the lira and Turkish equities, which are trading at a 40% discount to their emerging market peers. Recovery plays are to be found in financial services (Turkiye Garanti Bankasi) and chemicals (Petkim Petrokimya Holding).

Finally, Pakistan has been making progress, both in terms of political and economic stability. The new government elected this year seems willing to take unpopular measures, such as increasing gas tariffs, to improve the economy. With the IMF’s help, and if the promised fiscal reforms go ahead, the macroeconomic backdrop could quickly improve, leading to a possible rerating of the country’s equities, which are trading at a 7.1x forward P/E and 50% discount to the MSCI Emerging Market Index. Firms involved in infrastructure development and financial services could become interesting opportunities as confidence improves.

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document. (6)