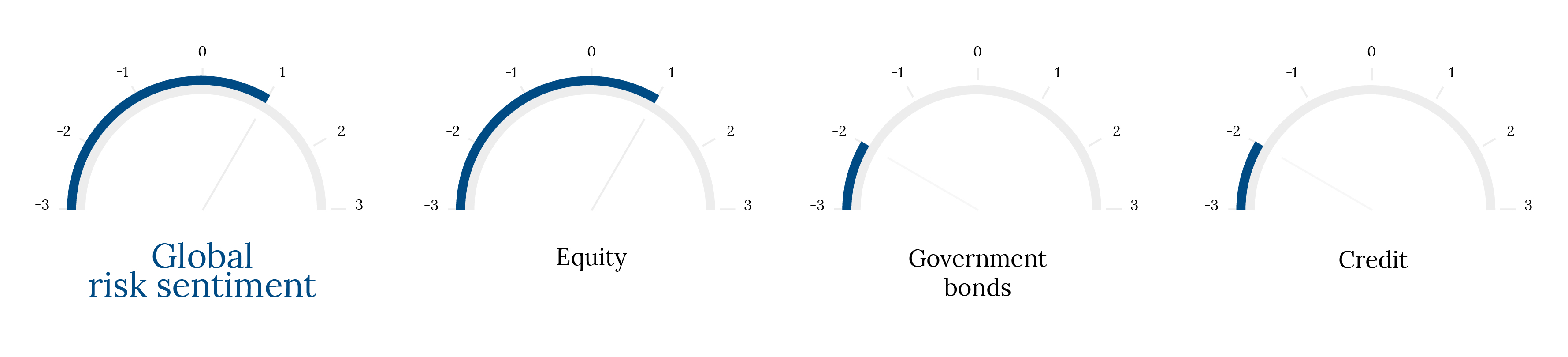

Sell in May and go away? It may be better to think twice. This is because nothing has really changed over the last month. While we remain concerned about expensive valuations across many asset classes, the current Goldilocks economic backdrop – acceptable growth without any inflationary pressures leading to gradual monetary policy normalisation – remains supportive of risk. Political uncertainty may remain the biggest unknown risk, if it’s large enough to lead to policy uncertainties. A political flashpoint could indeed occur at any point but is now more likely in the US than in the Eurozone, with the increasingly maverick President Trump at the helm. But even so, it is extremely difficult to pinpoint a policy tipping point or a market damaging global stand-off – whether it is simmering tensions in the Korean peninsula, terrorist attacks or a Trump tweet. All this taken into account, we are keeping a mild preference for risk, which will benefit from low volatility levels, while keeping some protection in place, in case of a correction. We believe there is a high probability this will occur in the next few months and we will use this opportunity to reload some risk at a better entry point.

Is it a case of history repeating?

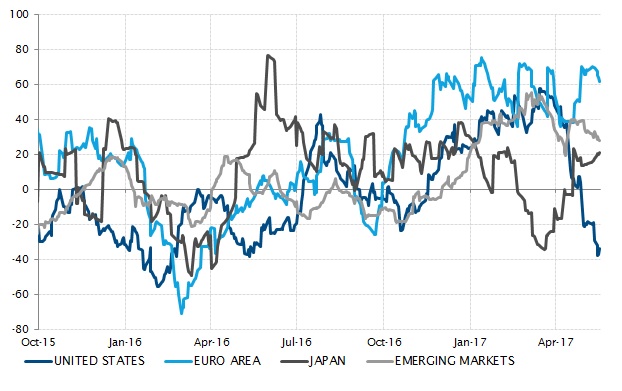

The current low-volatility environment of rising equity markets is reminiscent of the 2005-2006 period: expensive asset valuations, a euro-zone recovery, the euro regaining ground against the greenback, and the ECB on the eve of normalising its monetary policy. Despite commentators considering the current context as either new or exceptional, we strongly believe it may be a case of history repeating with a few amendments. The key differences are, firstly, the equity mania is not in EMs, but in the technology sector, which has consistently outperformed since mid-2013. More importantly, the debt level in the global system has increased further, impeding any significant increase in the overall level of interest rates without causing a crash (that will lead to the final "japanification" step of developed economies).

Volatility set to stay low

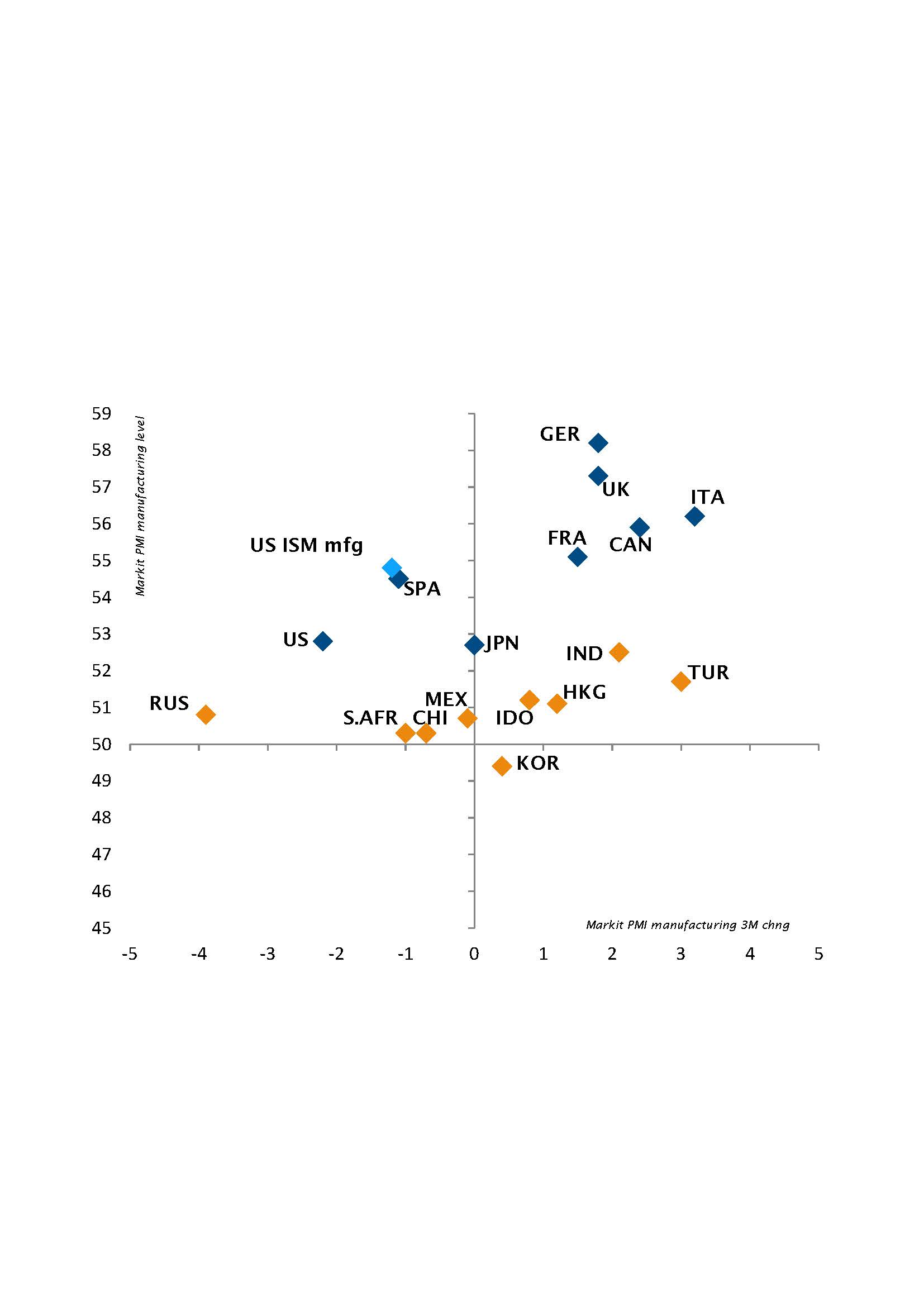

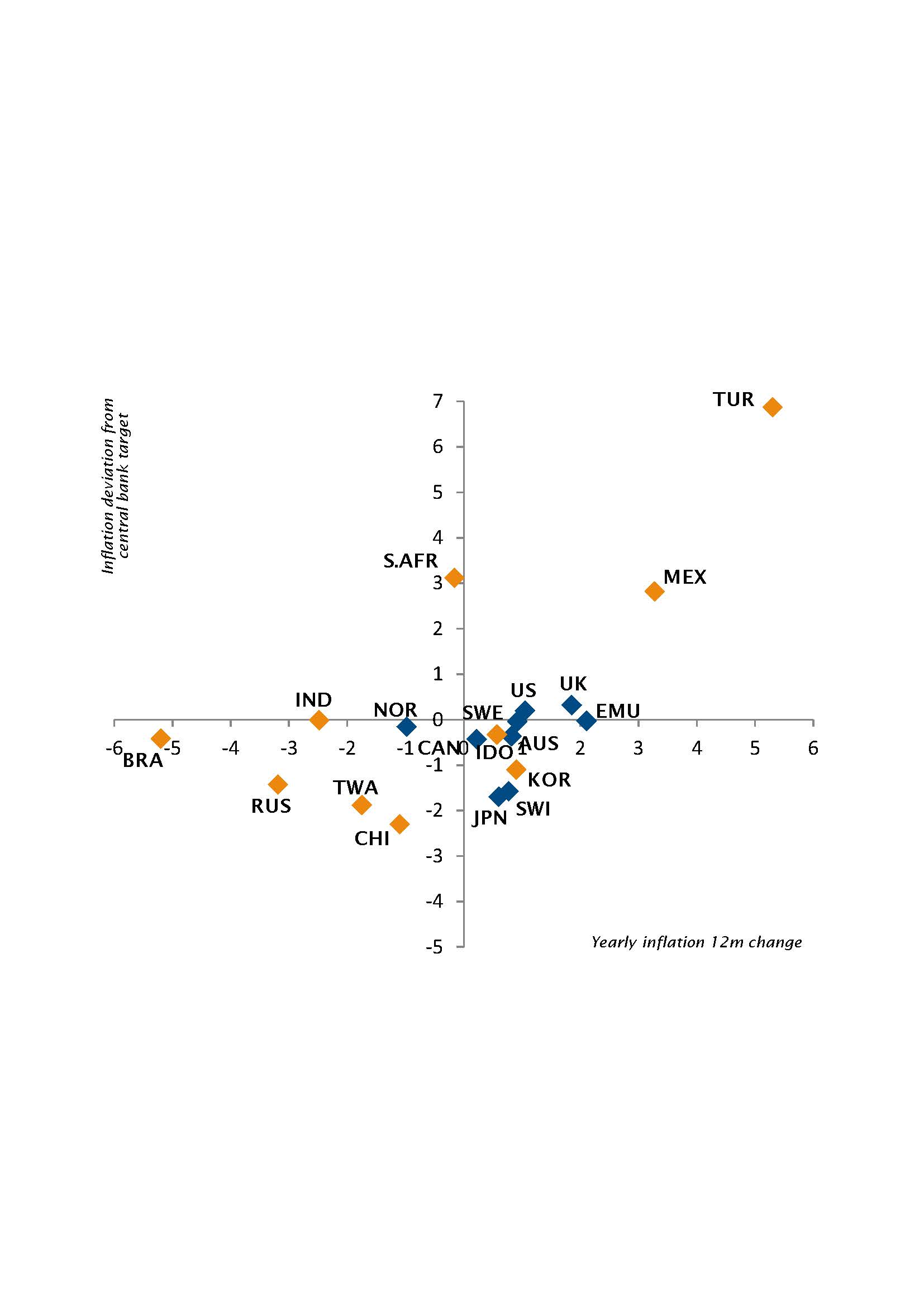

For the rest, it’s more of the same - equities risk premium and credit spreads were even tighter than today. As long as there is not a sufficient shock to derail the global economy or change, drastically, the path of the Fed’s monetary normalisation, volatility spikes won’t last much longer and overall volatility levels will remain low. In this context, we upgraded EM LatAm equities to a mild preference on the back of the correction triggered by the new Brazilian politics scandal, as the fearful contagion outside the Brazilian equities market was undue. Highlighting the similarities with 2005-2006, US long-term interest rates should thus remain quite stable. The only (temporary) upward risks in the foreseeable future will certainly arise not because of US growth acceleration or a sudden change in the Fed’s target rate path, but from a repricing of the German yield curve. It may now happen anytime soon, but the day of official reckoning from the ECB that their exceptional measures should be removed is coming. Thus we are keeping our tactical disinclination stance on duration, especially on German Bunds and JGBs. In the forex space, consistent with the views above, we believe the euro will continue to appreciate against the dollar and some carry trade positioning should get more crowded going forward. This is because some EM currencies, such as MXN or TRY, still offer rather cheap valuations with relative appealing absolute and relative yield, compared, for example, to the low expected returns of European HY which was downgraded to a disinclination last month. Similar to the upgrade in European equities last month, we continue to reshuffle our portfolio risks where we find some pockets of (relative) value.

_Fabrizio Quirighetti